TRANSACTIONS COST MATTER

Transaction costs are often overlooked as an influence on investment outcomes. Transaction costs are commonly divided into direct costs such as commissions, fees, and taxes while indirect costs include market impact and opportunity costs. Investment advisers widely accept that execution costs can reduce performance in a meaningful way. A recent study concluded the average annual transaction cost for a mutual fund in the U.S. was 1.44%[1]. Such costs really add up over time – 1.44% per year could lead to a 20% or more negative impact every decade.

All Atlas Capital Advisors, equity strategies are optimized to minimize transaction direct costs. Atlas manages approximately $1 billion in client capital, a large number in appearance, but not large in relation to the size of the markets we trade. We are large enough to be a meaningful counterparty on the platforms on which we trade but small enough to transact with minimal, if any, market impact. Such nimbleness is difficult to attain at larger firms. These execution costs can erode net returns and is one of the many benefits of using Atlas to implement an investment strategy.

We also control transaction costs by limiting the number of transactions. Atlas rebalances client holdings once per calendar quarter. The rebalance trades done for clients are only those which leave the client with a higher expected return than before, considering tax impacts for taxable clients.

ANALYZING THE MARKET IMPACT

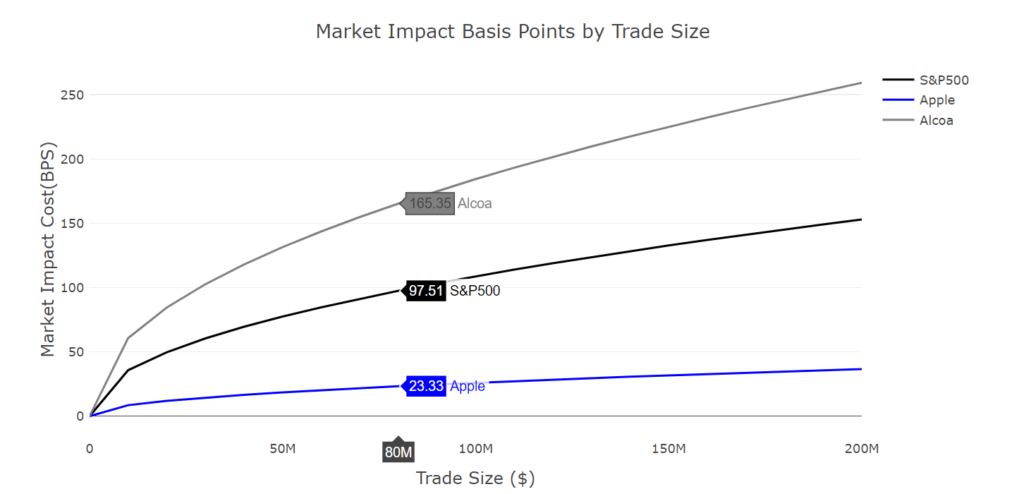

The biggest factors when estimating market impact, and ultimately investor execution costs, are transaction size and trading volume for the security in question. The chart below shows the estimated market impact by trade size for the average stock in the S&P 500, a high volume stock, Apple, and a low volume stock, Alcoa. The market impact for a $10 million dollar trade of an average S&P 500 stock is about 35 bps. That implied cost rises to about 130 bps for a $150 million dollar trade. Correspondingly, market impact costs are lower for higher-than-average volume stocks and more expensive for lower-than-average volume stocks. Intuitively, common sense supports the mathematical findings; it’s easier to be a price taker for proportionally smaller amounts of volume. Of course, any experienced trader will not execute substantial quantities of stock merely by executing market orders; they will work to mitigate their market impact by strategically working the amount of volume they want to trade using any variety of trading techniques (algorithm, VWAP, REL limit, etc). This now introduces another level of risk associated with time needed to execute; the market can move away from you thereby adding to the opportunity cost of execution. For those interested in additional data on this subject, please refer to a study in our database of External Research.

[1] “Scale effects in mutual fund performance: The role of trading costs,” Page 37. Accessed Jan. 18, 2021.