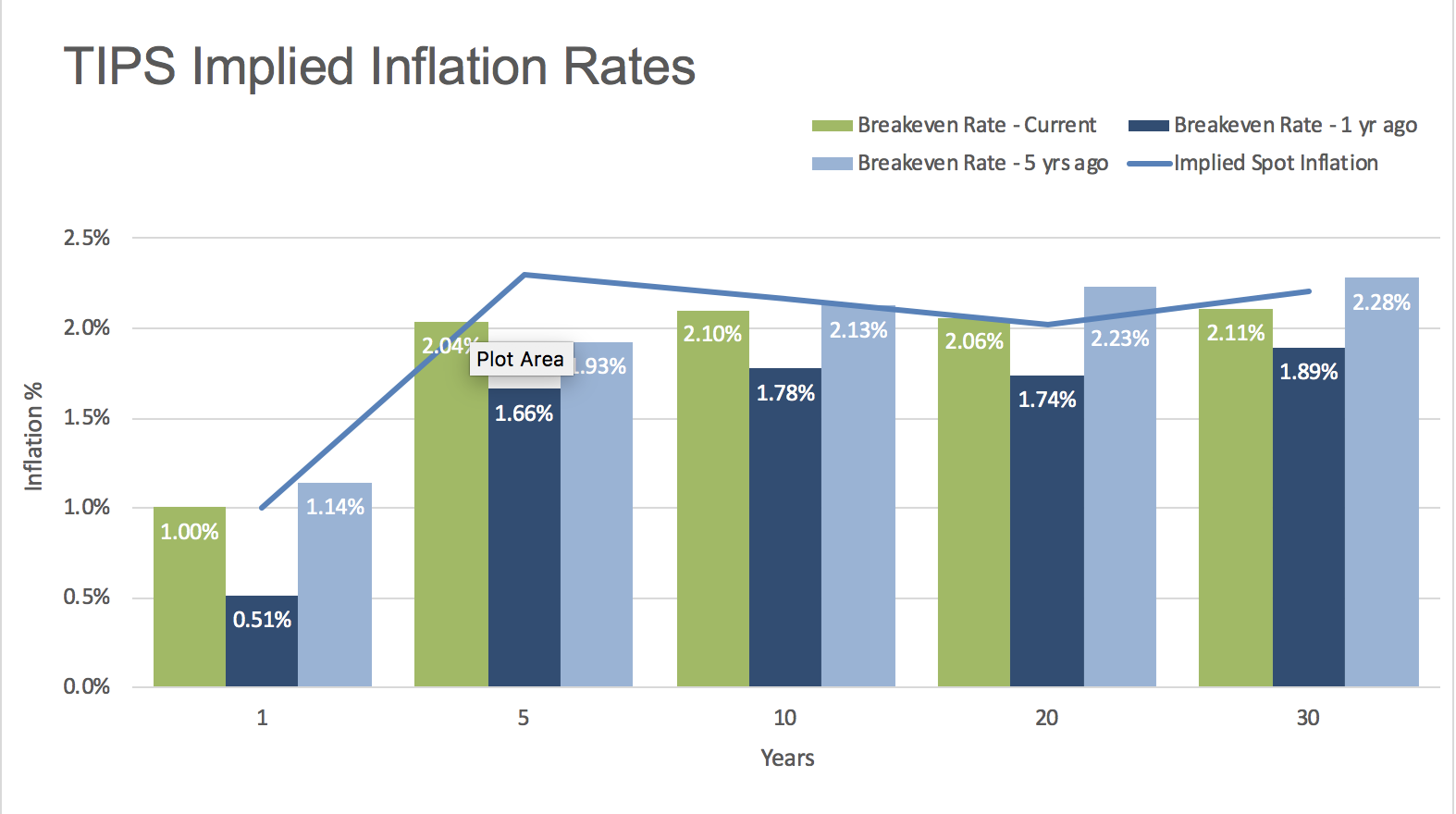

Bond investors should always be concerned about future inflation and how its effects can rob purchasing power from fixed income cash flows. A useful way to monitor market expectations for future inflation is analyzing “breakeven rates” along the yield curve. A breakeven rate is defined as the difference between a nominal bond yield and the yield of an inflation linked bond of the same maturity. This yield difference is essentially the breakeven inflation rate discounted by the market for the specified maturity term; it’s the rate at which an investor is indifferent between owning the nominal bond or owning the inflation linked bond. Simplistically, if the investor believes the market is underestimating future inflation, they would prefer to own the inflation linked security and vice versa if they perceived future inflation would be lower than market forecasts.

The deepest market for such securities is the US Treasury market which contains both nominal bonds and Treasury Inflation Protected Securities (TIPS) for varying maturities. Analyzing security prices for both asset classes we can 1) determine breakeven rates for various terms and 2) graph implied spot expected inflation rates for various points in time. Investing in nominal fixed income securities (eg: corporate and municipal bonds) should always be considered in the context of market expectations for future inflation.